Adoption and Purpose of the CSRD

The Corporate Sustainability Reporting Directive (CSRD) is a regulatory milestone introduced by the European Commission in November 2022. It replaces the Financial Reporting Directive (NFRD) and significantly strengthens social and environmental reporting rules.

The directive aims to support transparent decision-making for investors and stakeholders by introducing more comprehensive reporting requirements.

Additionally, it aligns with the goals of the European Green Deal by promoting sustainable business practices. This ensures companies across the EU meet higher sustainability standards.

The CSRD reflects the growing need for reliable Environmental, Social, and Governance (ESG) reporting.

For example, companies now have to disclose their sustainability impacts and risks through standardized frameworks like the European Sustainability Reporting Standards (ESRS). This allows for accurate comparability and transparency across industries.

Why Was the CSRD Introduced?

The CSRD was designed to address gaps in the non-financial reporting previously mandated under the NFRD. It empowers stakeholders, including investors and regulatory bodies, with robust ESG data to facilitate informed decision-making.

By requiring companies to adopt standardized reporting formats and disclose detailed sustainability metrics, the CSRD tackles challenges like greenwashing and ensures accountability.

Who Needs to Comply with the CSRD?

Scope and Applicability

The CSRD significantly broadens the scope of entities required to comply compared to its predecessor, the NFRD. Approximately 50,000 companies are now covered, a substantial increase from the 11,700 previously mandated.

Compliance is determined based on the following criteria:

- Companies with more than 250 employees.

- Businesses generating over €40 million in turnover.

- Total assets exceeding €20 million.

In addition to EU-based companies, non-EU firms generating over €150 million in the EU market must also report under the directive, ensuring a level playing field in sustainability practices.

SMEs and Large Companies

Both large enterprises and listed small and medium-sized enterprises (SMEs) are now required to comply. The phased implementation timeline accounts for varying company sizes, giving smaller businesses more time to adapt to the new requirements.

What Does the CSRD Require Companies to Report?

Double Materiality in Reporting

The CSRD introduces the concept of double materiality, which requires businesses to assess and report on:

- Financial Materiality: How sustainability issues affect the company’s financial performance and operations.

- Impact Materiality: The company’s impact on society and the environment.

For instance, logistics providers must assess how their operations contribute to emissions (impact materiality) while also evaluating how climate risks affect their long-term viability (financial materiality). This dual perspective ensures comprehensive accountability.

Standardized Reporting

All reports must align with the European Sustainability Reporting Standards (ESRS). These standards provide detailed guidance on the metrics and methods for sustainability disclosures.

Data must be submitted in a standardized digital format to enable comparability across EU member states. This requirement supports the EU taxonomy’s goals of fostering consistent and reliable sustainability assessments.

Third-Party Assurance

To enhance reliability, the CSRD mandates third-party assurance for all disclosed data. The European Financial Reporting Advisory Group (EFRAG) plays a pivotal role in defining these standards and ensuring uniform compliance.

Key Disclosure Areas

Companies are required to report on the following:

- Environmental protection.

- Social responsibility and employee treatment.

- Respect for human rights.

- Anti-corruption and bribery measures.

- Board diversity, including age, gender, and professional backgrounds.

- Risk management and opportunities related to sustainability.

How the CSRD Impacts Logistics and Supply Chains

Focus on Scope 3 Emissions

The CSRD emphasizes accountability for emissions across entire supply chains, including Scope 3 emissions. For logistics providers, this means assessing the environmental, social, and governance impacts of their operations, from transportation fuel consumption to warehousing practices.

Enhancing Transparency for Logistics Providers

By meeting the CSRD’s stringent ESG reporting requirements, logistics companies can enhance transparency, build trust with stakeholders, and align with global sustainability goals.

For instance, detailed reporting on CO2 emissions can position companies as leaders in sustainable logistics.

Leading Through Compliance

Adhering to CSRD requirements is an opportunity for logistics providers to differentiate themselves in a competitive market. Companies that embrace sustainability initiatives can leverage compliance to strengthen their brand and gain a competitive edge.

Challenges and Opportunities of the CSRD

Key Challenges

The CSRD brings with it a set of significant challenges that require careful navigation by companies. One of the most demanding aspects is conducting rigorous double materiality assessments.

This involves evaluating how sustainability issues impact a company’s financial performance while simultaneously analyzing the company’s effects on the environment and society. This dual perspective requires detailed data collection and nuanced analysis, which can be resource-intensive.

Additionally, adjusting internal processes to align with standardized reporting formats set out by the European Sustainability Reporting Standards (ESRS) can be complex. Many companies will need to overhaul existing workflows, invest in new systems, and train staff to ensure compliance with these rigorous requirements.

Finally, the mandate for third-party assurance introduces an added layer of accountability, necessitating high levels of accuracy and reliability in all reported data. This can be a daunting task for businesses new to sustainability reporting.

Strategic Opportunities

While the challenges are considerable, the CSRD also unlocks substantial opportunities for forward-thinking businesses.

Adhering to CSRD requirements, companies can significantly enhance their credibility and transparency.

This transparency not only builds trust with investors and stakeholders but also positions companies as leaders in sustainability within their industries.

Moreover, aligning business strategies with the European Green Deal’s sustainability goals can unlock long-term benefits. Companies that integrate environmental, social, and governance (ESG) principles into their core operations are better equipped to adapt to regulatory changes and evolving market demands.

For logistics providers, the directive presents a unique chance to showcase leadership by adopting robust ESG practices.

Embracing these changes strengthens brand reputation and opens new market opportunities, particularly as customers and partners increasingly prioritize sustainability in their decision-making.

Practical Steps to Prepare for CSRD Compliance

Start Early

Companies should begin compliance preparations as early as possible to avoid last-minute hurdles. Early action enables businesses to identify gaps and address them systematically.

Build Robust Reporting Systems

Investing in advanced systems for data collection, management, and reporting is crucial. These systems should, of course, align with the ESRS and support double materiality assessments.

Collaborate with Experts

Engaging external advisors and auditors can streamline the compliance process. Insights from the Financial Reporting Advisory Group (EFRAG) can guide companies in meeting assurance requirements.

Leverage Technology

Platforms like Dockflow can simplify the process of tracking ESG metrics and preparing comprehensive management reports. Dockflow’s solutions are particularly valuable for logistics providers aiming to achieve CSRD compliance efficiently.

You can explore Dockflow’s RealCalc and more about Dockflow’s reporting features on our CO2 Tracking page.

Timeline for CSRD Implementation

Meeting the CSRD reporting requirements involves adhering to a phased timeline that varies depending on company size and type.

These deadlines ensure a smooth transition for businesses while maintaining the directive’s overall goals of transparency and sustainability.

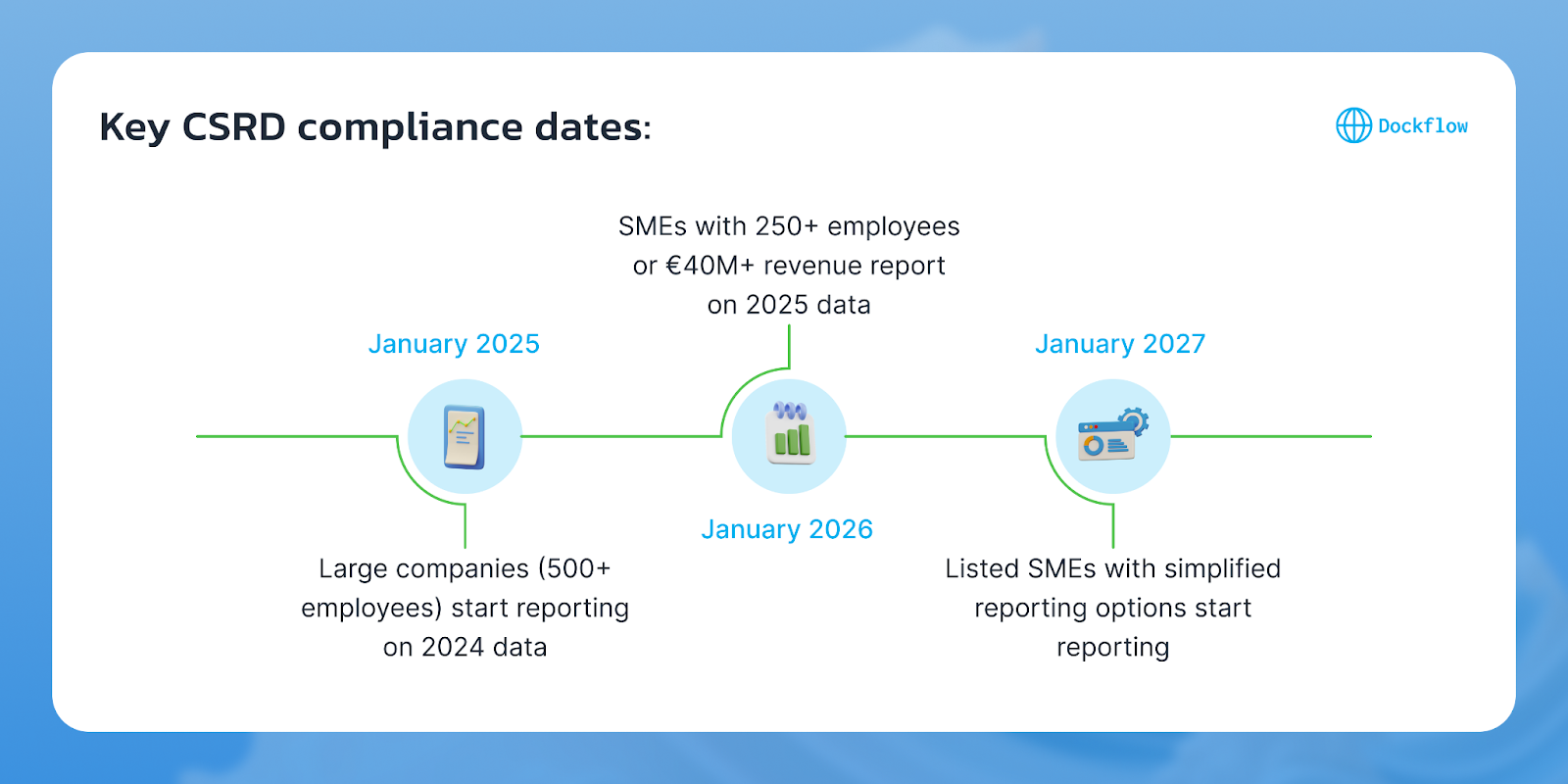

- 2024: Companies currently under the NFRD are required to report on their FY 2024 data, which will be published in 2025. This marks the initial phase of integrating the enhanced CSRD standards for entities already accustomed to non-financial reporting practices.

- 2025: Large companies not previously covered by the NFRD will need to begin reporting on their FY 2025 data, publishing the reports in 2026. This expansion significantly increases the number of entities adhering to standardized sustainability practices.

- 2026: Listed small and medium-sized enterprises (SMEs) and small financial institutions must report on their FY 2026 data, with publication in 2027. This stage acknowledges the need for smaller businesses to have additional time to adapt to the directive’s rigorous requirements.

- 2027: Non-EU companies that generate over €150 million in the EU market must report on their FY 2027 data, publishing the reports in 2028. This inclusion ensures a level playing field and extends the CSRD’s impact beyond EU borders, promoting global sustainability accountability.

Why CSRD Matters for the Future of Sustainability

Driving Global Change Through Corporate Responsibility

The CSRD drives corporate responsibility by aligning financial and operational strategies with global ESG goals. It fosters a transparent and accountable business environment.

Long-Term Benefits for Businesses

By adhering to the CSRD, businesses can build resilience in a sustainability-focused economy. The directive ensures companies stay ahead of evolving regulatory expectations while strengthening market trust through compliance with the EU taxonomy and ESG principles.

How Dockflow Supports CSRD Compliance

Streamlining Sustainability Reporting with Dockflow

Dockflow provides logistics companies with innovative tools to simplify compliance with the Corporate Sustainability Reporting Directive (CSRD). By integrating advanced technology and actionable insights, Dockflow ensures businesses meet the directive’s stringent requirements efficiently.

The CSRD mandates detailed disclosures across environmental, social, and governance (ESG) criteria. Dockflow’s RealCalc® is designed to address these needs, combining real-time data tracking, automated reporting, and comprehensive analytics tailored for the logistics industry.

Leveraging RealCalc® for CO2 Tracking and Reporting

Real-Time Emissions Monitoring

RealCalc®, Dockflow’s CO2 emissions tracking tool, provides logistics providers with precise, real-time data on their carbon footprint. By leveraging satellite tracking, fuel consumption metrics, and operational data, RealCalc® enables companies to:

- Monitor Scope 1, 2, and 3 emissions.

- Identify high-impact areas for targeted sustainability efforts.

- Ensure compliance with the European Sustainability Reporting Standards (ESRS).

Automated Data Collection and Reporting

One of the challenges of CSRD compliance is gathering and presenting data in a standardized format. RealCalc® automates this process by:

- Aggregating data from multiple sources, including shipping routes, fuel usage, and warehouse operations.

- Generating reports aligned with EU taxonomy requirements.

- Ensuring third-party assurance readiness with accurate and verifiable data.

This automation reduces the administrative burden, allowing logistics teams to focus on strategic sustainability initiatives rather than manual data entry.

Predictive Analytics for Proactive Compliance

RealCalc®’s predictive analytics feature helps businesses anticipate potential compliance risks and opportunities. By analyzing historical data and market trends, the tool can:

- Forecast emissions based on planned routes or operational changes.

- Suggest optimized shipping schedules to minimize environmental impact.

- Highlight areas where further investment in sustainability is needed.

Integration with Supply Chain Partners

Dockflow’s collaborative tools allow logistics companies to work closely with supply chain partners to improve overall ESG performance. By sharing emissions data and sustainability metrics in real-time, businesses can:

- Align goals with partners.

- Ensure collective compliance with CSRD standards.

- Foster a culture of accountability and continuous improvement.

Why Dockflow is the Ideal Partner for CSRD Compliance

Dockflow is more than a technology provider; it is a strategic partner for logistics companies navigating the complexities of sustainability reporting. With tools like RealCalc® and a deep understanding of CSRD requirements, Dockflow helps businesses:

- Achieve regulatory compliance efficiently.

- Enhance their ESG performance and market reputation.

- Build resilience in a rapidly evolving industry focused on sustainability.

By choosing Dockflow, logistics providers can turn CSRD compliance from a regulatory challenge into a competitive advantage, showcasing their commitment to environmental and social responsibility while staying ahead of industry trends.